Maciej Ulaszewski

Maciej Ulaszewski

One of the frequently highlighted advantages of low-code platform is its ability to accelerate and reduce costs of application development. Consequently, within the programming community, this technology is predominantly linked to testing business ideas, crafting MVPs, and developing internal solutions for organizations. However, advanced low-code platforms enable the creation of enterprise‑grade applications that rival those developed using traditional methods and can be seamlessly deployed for end users. In the banking industry, low-code platforms are driving innovation and competitiveness, enabling banks to stay competitive in a rapidly changing digital marketplace, improve speed and efficiency of software development, bridge the talent gap, empower internal users to innovate, deliver personalized experiences to customers, ensure compliance, and improve the overall security of their systems.

Yet, challenges persist. Specifically within the banking realm, these challenges primarily revolve around meeting evolving customer needs and expectations that drive industry trends. Additionally, there are internal challenges concerning banks themselves, encompassing integration within the bank’s ecosystem, the sustainability and scalability of solutions created, and ensuring adherence to regulatory standards.

This article aims to delve into the primary challenges encountered in low-code development of customer‑facing solutions, while also suggesting the requisite benchmarks banks should seek in a low-code platform to address these challenges.

Customers prioritize intuitive interfaces and user-friendly banking apps. The initial challenge lies in seamlessly integrating components crafted through low-code into traditionally programmed applications for efficient app development, ensuring both UI/UX uniformity and comprehensive functionality. This integration accelerates the development process, enabling banks to innovate and customize workflows for digital banking services, customer service apps, and business processes automation.

A competent low-code platform should offer not just a repository of front‑end components but also the flexibility to customize the appearance and operations of these components. This customization ensures harmony between low-code solutions and the native elements present in the application.

Given that components tailored for browser‑based applications might not work in mobile apps (owing to smaller screens and touch‑based operations), a proficient low-code platform must facilitate replacing these elements with more suitable ones designed for mobile applications.

Customize the appearance and operations of components with a low-code platform

Equally critical is the framework that, based on the style guide, establishes standards ensuring both stylistic uniformity and functional coherence across solutions. This framework provides clear guidelines for low-code developers to configure components and seamlessly integrate them into existing applications.

Ideally, the platform should facilitate integration, enabling one‑off customization of UI/UX while ensuring security and technological compatibility. It eliminates the need to address these aspects repeatedly when creating or modifying subsequent business applications.

Moreover, the low-code platform should guarantee the extensibility of the user interface to align with the bank’s specific business requirements. For instance, this might involve incorporating an SFCS survey or a component allowing customers to personalize graphics on their payment cards. Consequently, the platform must empower low-code teams to develop components internally and utilize those offered by third‑party vendors.

Adding a component on a low-code platform

The platform should enable the creation of various process elements seamlessly integrated with the application’s functionalities. For instance, if the application employs biometric authorization for customer‑initiated transfers, the same method should be upheld consistently within the low‑code‑created application.

In September 2023, Santander Bank launched the new mobile application, a collaborative effort involving teams across multiple countries. This app caters to Santander customers in Poland, the UK, Spain, and Portugal, and it is tailored meticulously to meet the specific needs of each market. It succeeded the previous Santander Mobile application, which featured 30 forms crafted using the Eximee Low-Code Platform.

All forms previously available on Santander Mobile seamlessly transitioned to Santander OneApp with changed and unified branding. Leveraging the Eximee platform’s ability to separate the frontend layer from the business logic, there was no necessity to recreate forms from scratch. Instead, a single adaptation of the interface to the new style guide sufficed for all forms, preserving the underlying business logic intact.

This approach not only expedited the project timeline but also significantly curtailed the expenses incurred for alterations. It serves as a testament to the longevity of low-code applications in the banking sector, where rapid modifications are commonplace, showcasing their extended lifecycle compared to traditionally developed frontends.

The screenshots below illustrate changes – the left depicts a screen from the Santander Mobile app, while the right showcases the Santander OneApp interface.

Comparison of Santander Mobile vs. Santander OneApp

Comparison of Santander Mobile vs. Santander OneApp

Customers engage with banks through varied channels—some prefer in‑person visits to branches, while others opt for mobile apps or websites. Multichannel functionality empowers customers to choose their preferred interaction mode at any time. However, integrating application elements across these channels necessitates ensuring consistent UI/UX experiences throughout the process. This approach notably benefits business users by enabling them to participate in the development process across various channels, leveraging low-code platforms to contribute effectively without needing extensive coding knowledge.

Certain low-code platforms offer the capability to create a unified solution for multiple channels while allowing frontend customization to meet specific channel requirements and user preferences.

In practice, this means that low-code developers need not tailor a solution for a particular channel. Utilizing a framework alongside reusable graphical components, integrations, and business logic, the styling and behavior of the solution remain consistent across all channels. However, the arrangement of graphical elements on the screen adjusts responsively based on the channel and device displaying it.

Furthermore, an efficient low-code tool facilitates simultaneous changes across all channels. This feature negates the necessity to embed a given service separately in various locations, streamlining the modification process.

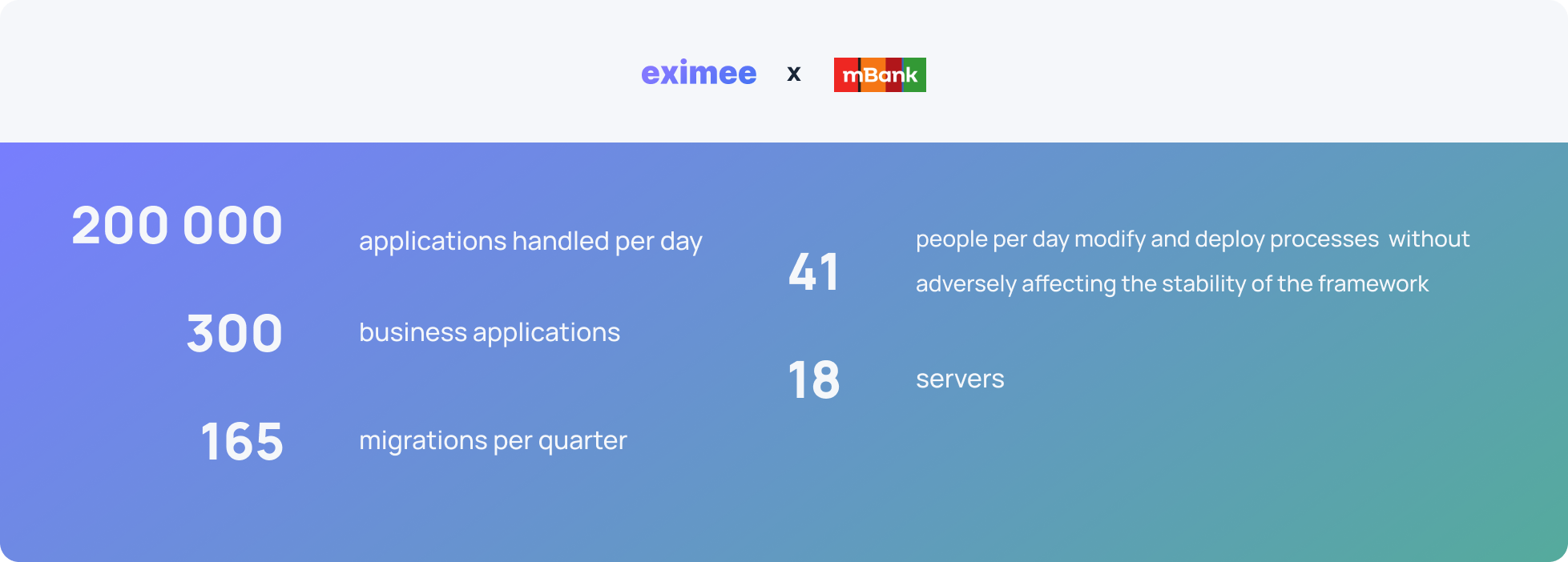

mBank harnesses the Eximee Low-Code Platform to craft forms shared across multiple channels. The visual aesthetics remain uniform, yet the arrangement of individual elements is tailored to suit each channel’s specifications.

Shown below is the view displayed on online banking and the website for non‑logged‑in customers (left), juxtaposed with the view within the mobile application (right).

, and the mobile application (right)")

The views displayed in online banking and the website for non-logged-in customers (left), and the mobile application (right)

Here’s a glimpse of the view of the application for bank employees: when the screen is shared, customers exclusively view the right section, while the left side enables employees to take notes. For instance, they might jot down the loan rate agreed upon during the conversation with a customer.

The view of the application for bank employees

Customers expect seamless switching between channels without losing their case context or entered data. For instance, they may begin a loan application in a mobile app and wish to conclude it via online banking or a phone call to a call center. Additionally, they demand prompt access to case status information, irrespective of the channel they used to contact the bank.

To fulfill these expectations, you need a platform that provides easy and secure integration of existing channels (e.g., online banking, mobile banking, branch applications and call centers). Furthermore, a unified data model is essential, facilitating smooth data flow across channels and enabling synchronization and aggregation of data collected from processes in all channels. The importance of security in omnichannel integration extends to protecting customer data, ensuring that sensitive customer data is safeguarded through automated compliance tasks and reducing the risk of human error.

The low-code platform should empower users with continuous control over ongoing processes. It should offer insights into which channel the case originated (e.g., mobile app), its current processing channel (e.g., branch), and its current status, ensuring both bank employees and customers have constant access to real-time data and statuses.

Control over ongoing processes on Eximee Low-Code Platform

The low-code platform should also register the channel through which the bank acquired customer information or consents pertinent to the process. For instance, knowing whether a customer provided consent independently or through a specific employee can be crucial when addressing disputes.

In scenarios involving intricate business processes, different process stages may be available in particular sets of channels. For instance, in the mortgage renegotiation process at one of the Polish banks, customers can initiate mediation requests through online banking, the mobile app, at branches, or via the call center, based on their preferences.

The essential step in the process is negotiation with the customer, typically occurring in a branch or during an online meeting. The mediator enters data and agreement specifics into the system using a dedicated form. Subsequent steps are managed by the back office, and the signing of the documents takes place at the bank’s branch, as required by the regulator.

Forms embedded in the process can be displayed in different ways depending on the channel, e.g., forms for a call center employee and a branch employee can contain different fields. Nonetheless, filling out a form constitutes a uniform step within the process, yielding the same outcome regardless of the channel used. Moreover, the Eximee platform enables comprehensive case status tracking across all channels.

Uniform step within the process in filling out a form

E-commerce has set a precedent for quick and convenient shopping, conditioning consumers to expect uninterrupted access to products and services from various sectors, including banking. Customers now demand hassle-free banking experiences, and efficient and dependable customer service, all with minimal paperwork. They seek immediate activation of banking products post‑purchase and expect banks to anticipate their preferences, offering personalized services and products precisely when needed, e.g., an instant cash loan when a customer attempts a card payment without sufficient funds reflects this expectation. The solution to meeting these demands lies in process automation. In the banking sector, efficient account management is significantly enhanced by automation, which streamlines operations, reduces errors, and accelerates service delivery, meeting customer demands more effectively.

Seek out a low-code platform capable of swiftly crafting business logic for processes, enabling agile responses to evolving customer needs. A low-code developer should be able to independently write scripts to, for example, calculate the cost of a loan according to a provided formula, or specify conditions that determine whether a field on a form should display or not.

The capacity to rapidly prototype solutions and deploy them in a test environment is paramount. In essence, this means crafting a functional application from the project’s inception and later expanding its capabilities.

The forefront low-code platforms facilitate continuous deployments, allowing swift and seamless alterations or additions to functionalities independent of the bank’s release cycle. These changes occur without disrupting the availability of products and services to customers. By ensuring uninterrupted process availability, banks gain the agility to more flexibly align their offerings with both customer expectations and regulatory demands, including automating compliance processes to improve regulatory compliance and reduce the risk of errors and non-compliance.

The low-code platform should provide easy integration with the banking system and applications and services provided by other vendors. As a result, it must offer cohesive APIs facilitating integration with internal systems (e.g., customer files, card processing systems), services (e.g., OCR), and external services (e.g., identity verification, loan origination).

For efficient and cost‑effective process automation, consistent support for automated processes, and building a library of ready‑to‑use automations, choose a low‑code platform that allows separation and reusability of sub‑processes.

Additionally, seek a platform that provides Software Development Kits (SDKs) and a mechanism for implementing automated steps using low-code approach. This should include guidelines for defining business logic through scripts or microservices.

Low-code business process automation offers various approaches. One option involves automating entire processes from start to finish, while another focuses on automating specific critical steps that recur across multiple processes. In the case of a process for handling customer communications at Santander Bank, we chose the latter method and automated the step of sending emails with documents to customers.

The bank identified the previous document‑sending procedure as excessively time‑consuming. The agents were individually responsible for compiling and sending the documents to be delivered to a client in a given process. They had to download sample documents from the repository and ensure they were up to date, adding complexity to the process and elevating the risk of errors.

Presently, the Eximee platform provides employees with information on:

The document sending process underwent testing in various contexts, scenarios, and channels.

Streamlining the identical steps found in many processes is good practice. The repetitive part of the process is automated once, so the work is not duplicated by the teams responsible for particular processes.

By automating the document sending process:

A low-code platform should fit into the organization’s IT infrastructure and enable the development of maintainable and scalable applications while adhering to a bank’s standards and software production process, enhancing risk management by managing risks associated with application development.

The best low-code platforms have almost unlimited integration capabilities to leverage previously implemented solutions. If a bank uses a BPM system, such as Camunda, the low-code tool should integrate with it rather than force the engine change. In addition, a properly selected low-code platform provides the opportunity to construct business logic using internal services (e.g., document generation method, signature handling, authorization).

The architecture of a low-code platform should also provide the freedom to scale, that is, to multiply the capacity of processes by adding more instances. Expecting increased traffic in a particular process for a certain period of time, you can increase the “capacity" for this process by administratively allocating resources among processes. Conversely, when traffic diminishes, maintaining excessive resources becomes inefficient. Hence, the platform needs to facilitate dynamic resource management by scaling down and up as required. Low-code platforms streamline the software development process, making it more efficient and accessible.

An effective low-code platform safeguards against unforeseen performance issues by implementing process separation. This ensures the autonomy of different processes; for instance, separating loan servicing from onboarding. In the event of a process malfunction, it won’t disrupt other processes on the platform. This separation also mitigates the impact of designer errors; an issue in an account application won’t affect the cash loan sales process, for instance.

A pivotal capability offered by a low-code platform in banking is the provision of robust business analytics. Tailored analytical tools enable the tracking of conversion rate fluctuations over time, empowering prompt reactions to declines.

The accessibility of continuously updated data streamlines decision‑making for banks, enhancing their adaptability to market shifts and customer requirements. This flexibility significantly bolsters competitiveness by enabling the alignment of solutions with evolving market and customer dynamics.

Line graph from Eximee Low-Code platform

Through a meticulous analysis of the sales funnel, banks can pinpoint specific friction points within the process. These friction points represent instances where customers encounter challenges while interacting with the bank. Identifying these critical points offers banks an opportunity to concentrate on optimizing the steps that lead to the highest customer attrition, thereby enhancing customer experience and retention.

Bar graph from Eximee Low-Code Platform

Dashboard from Eximee Low-Code Platform

Low-code platforms tailored for banking offer the advantage of monitoring both the quality of business process handling and employee workloads. A well‑configured dashboard can furnish details such as ongoing and completed processes, task assignments per employee, average wait times for task processing, or average task handling time. Additionally, it enables tracking the volume of concurrent processes, number of service calls, and average wait times for automated task execution.

Another important aspect is the transparency of processes facilitated by graphical modeling, comprehensive documentation created directly in the tool, version difference tracking, and change attribution. A low-code developer without programming skills can implement substantial changes without disrupting dependencies.

As banks make their applications available to millions of end users, ensuring robust security becomes paramount when selecting a low-code platform. This platforms play a crucial role in enhancing the security and stability of banking applications by allowing for the creation of secure, custom applications even by those without technical expertise.

It is worth narrowing down the choice to enterprise‑class solutions dedicated to the banking sector. These platforms provide advanced security protocols aligned with industry standards and regulatory requirements. Moreover, they offer a framework ensuring security during the implementation of changes within production environments. If a bank already has effective safeguards against data breaches or denial of service attacks, a low-code platform can use the same solutions and certificates.

Moreover, the provider of the low-code platform should guarantee adherence to OWASP Top10 guidelines, conducting routine security tests, and subjecting their solution to third‑party audits to ensure continuous compliance and fortified security measures.

In today’s financial landscape, embracing advanced low-code platforms has emerged as a pivotal success driver. Banks opting for investment in low-code solutions can anticipate substantial reductions in both time and costs associated with developing end‑user applications. Furthermore, low‑code empowers them to adeptly execute omnichannel strategies, craft distinctive customer experiences, and personalize offerings to cater to individual customer needs. Nevertheless, the creation of low‑code applications poses specific challenges, underscoring the critical importance of selecting the appropriate tool for the task at hand.

The optimal choice for the banking sector often lies in a low-code platform specifically tailored to the industry’s nuances and requirements. One such exemplary solution is the Eximee Low-Code Platform, offered by Consdata S.A. We boast extensive experience collaborating with major banks in Poland, providing invaluable support for their digital transformations and omnichannel sales initiatives.

The team behind the development of the Eximee Low-Code Platform possesses deep insights into the intricacies of banking and comprehends the challenges confronted by financial institutions. This knowledge elevates Eximee beyond being solely a robust tool for application development and business process automation. It stands as a strategic partner dedicated to assisting banks in realizing their business objectives. Additionally, integrating low-code platforms into customer relationship management systems can significantly enhance CRM capabilities in banking, enabling non-technical staff to contribute to app development and automate workflows efficiently.

Low-code platforms help banks accelerate application development, reduce costs, and enhance competitiveness by enabling rapid innovation and streamlined processes.

Low-code platforms offer customizable components that can be seamlessly integrated with native applications, ensuring UI/UX uniformity and comprehensive functionality across digital banking services.

Multichannel support allows customers to interact with banks through various channels, ensuring consistent UI/UX experiences.

Low-code platforms adhere to industry standards and regulatory requirements, offering advanced security protocols and continuous compliance monitoring to protect customer data and ensure application stability.

Low-code platforms provide scalable architecture and robust business analytics, enabling banks to manage resources efficiently and adapt to market changes while maintaining application performance and reliability.